We’ve Been Speaking it Wrong

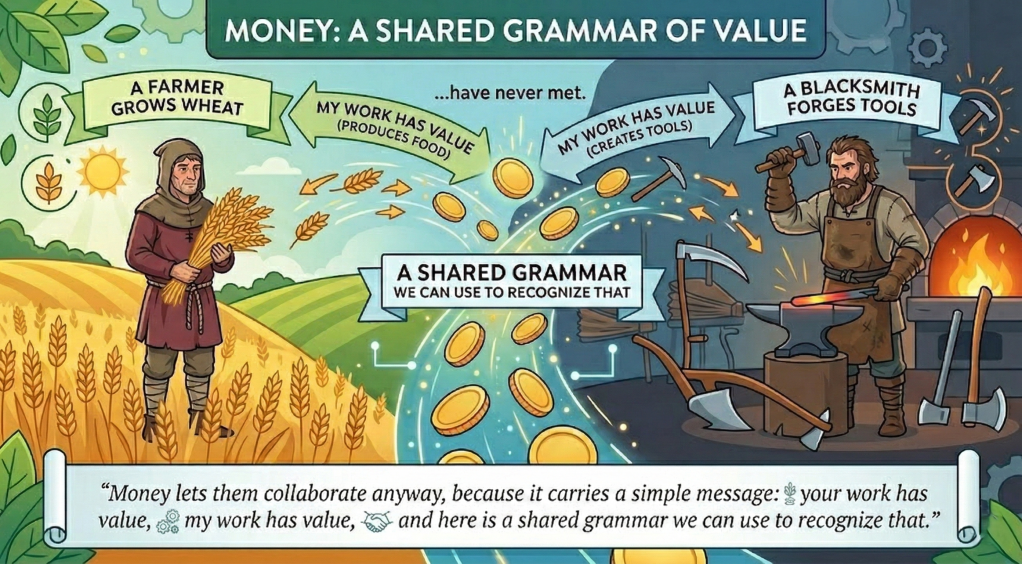

Money is a cooperative technology. That’s what it was built to do. Before it was a commodity, before it was a policy instrument, before it was a weapon, money was the language that let strangers work together without needing to trust each other personally. A farmer grows wheat. A blacksmith forges tools. They have never met. Money lets them collaborate anyway, because it carries a simple message: your work has value, my work has value, and here is a shared grammar we can use to recognize that.

This is so fundamental that we forget it. We think of money as something you earn, spend, save, invest. Something that moves between people. But before it moves, it speaks. It says: I see what you did, and it mattered.

The earliest money we know about wasn’t coins. It was ledgers. Clay tablets in Mesopotamia, roughly five thousand years ago, recording obligations within a community. This farmer contributed grain to the storehouse. This builder repaired the canal. The tablet wasn’t tracking exchanges between adversaries. It was tracking contributions among participants in a shared project called “we all survive this year.”

Money was the memory of cooperation. That’s all it was.

So what happened?

Somewhere along the way, we stopped saying “cooperation” and started saying “transaction.” And that shift wasn’t cosmetic. It was architectural.

Feel the word. Trans-action. Action across a boundary. The moment you frame money as transactional, you’ve introduced a boundary between the participants. Now there are two sides. Now there’s a buyer and a seller. Now someone got the better deal and someone didn’t. Now there’s information worth hiding, because if I know something you don’t about what we’re exchanging, I win.

The entire vocabulary of commerce lives inside this frame. Leverage. Arbitrage. Competitive advantage. Information edge. Proprietary data. Trade secrets. None of these words exist in a cooperative grammar. Every one of them is native to a transactional one.

And the transactional frame didn’t emerge because people got greedier. It emerged because someone captured the ledger.

Go back to those Sumerian clay tablets. The temple controlled them. And the moment a third party controls the memory of cooperation, that third party can edit the memory. They can add a line that says the temple is owed a percentage of every contribution. Not because the temple grew grain or dug canals, but because the temple keeps the record.

The temple becomes the first intermediary. And the intermediary needs a justification. So the framing shifts. It is no longer “we are all contributing to a shared project.” It becomes “you owe the temple, and the temple owes you, and these are separate accounts.” Two sides. A boundary. A transaction.

Cooperation doesn’t need a middleman. Transactions do. So the middleman reframes cooperation as transaction, and suddenly the middleman is essential.

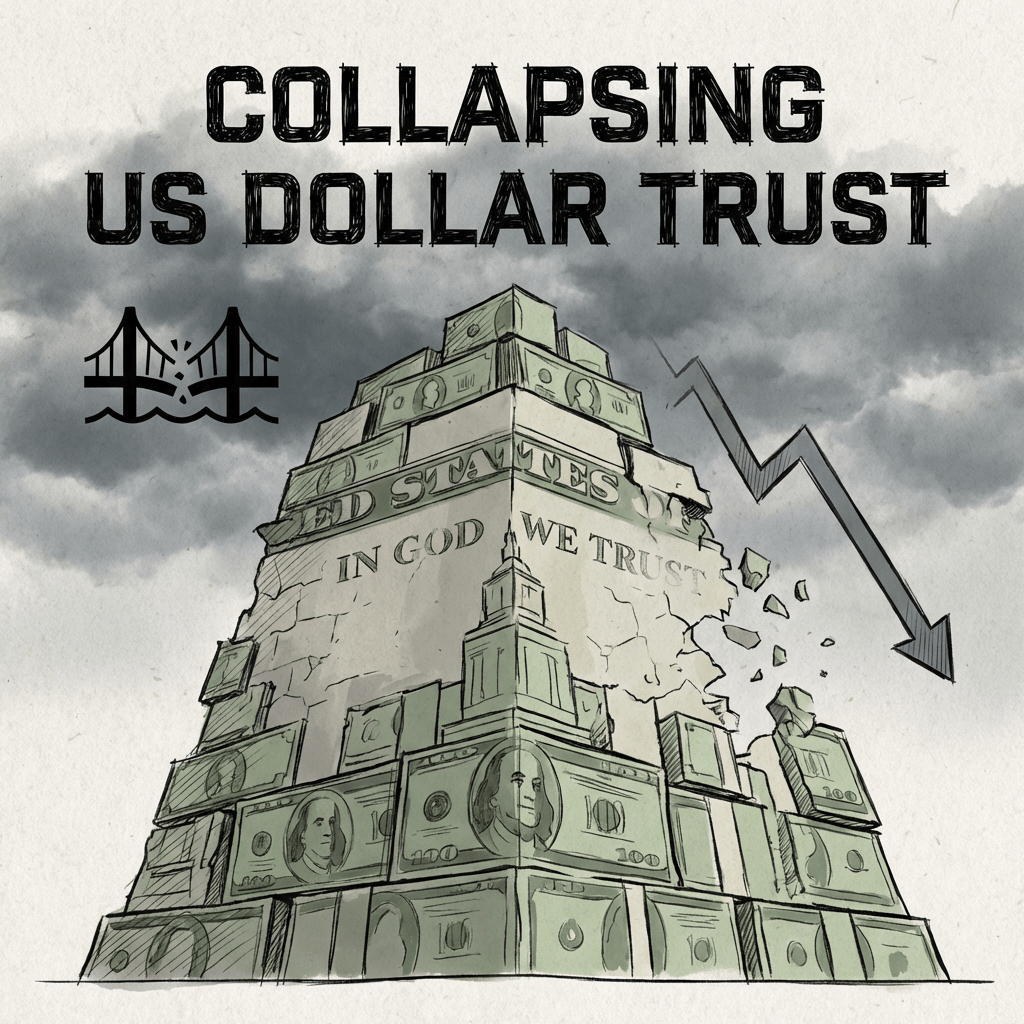

Every monetary system since has repeated this move. Rome puts Caesar’s face on the coins, routing every exchange through imperial authority. Medieval Europe routes commerce through the Church and the crown. The Bank of England. The Federal Reserve. Same architecture across five millennia. A third party inserts itself into the cooperative language, reframes it as transactional, and extracts rent from the reframing.

And here is the part that matters: every time the ledger keeper gains control, secrecy follows. Not as corruption. As structure.

The temple priests knew things about the community’s obligations that the community didn’t know about itself. That information asymmetry was the source of their power. Every intermediary since has operated on the same principle. Your bank knows your balance, your debt, your payment history, your risk profile. You don’t know theirs. The asymmetry isn’t a flaw. It’s the product.

Once the grammar is transactional, secrecy becomes rational. You’d be a fool to show your hand in a negotiation. You never reveal your cost basis. You never let the other side know how badly you need the deal. The language itself teaches you to hide.

And this is where the story connects to the headlines.

Jeffrey Epstein sat exactly where the temple priests sat. At the ledger. He knew who owed what to whom, who had been where, who had done what. He was the keeper of a private record of obligations, and that record gave him power over everyone in it. The powerful came to his table for the same reasons powerful people have always come to such tables: access, introductions, money, favors. The transactional grammar that governs our world made his position not just possible but inevitable.

People want to call Epstein an aberration. A monster who broke the system. But the system wasn’t broken. The secrecy didn’t emerge because people are bad, although bad people are certainly attracted to this sort of arrangement. The secrecy emerged because the structure demands it. Epstein didn’t break the system. He industrialized it.

Before Epstein, the same output was produced in smaller batches. Royal courts. Gentlemen’s clubs. Private salons where favors were traded and secrets accumulated by whoever controlled the guest list. The product was always the same: leveraged secrecy in a transactional grammar. Epstein built the factory.

And here is the question that should keep us up at night. Not “how do we prevent the next Epstein?” but “what kind of monetary language keeps producing them?”

Because the answer to the first question is always the same. More regulation. More oversight. More committees. More inspectors. And every single time, the people who control the transactional language co-opt the reformers. They hire the regulators. They fund the campaigns of the overseers. They donate to the institutions that are supposed to hold them accountable. This is not conspiracy. This is the language working as designed. In a transactional grammar, the most fluent speaker always wins.

The answer to the second question is different. It asks us to look at the grammar itself.

What if the language of money could return to its cooperative roots? Not through legislation or moral improvement, but through design?

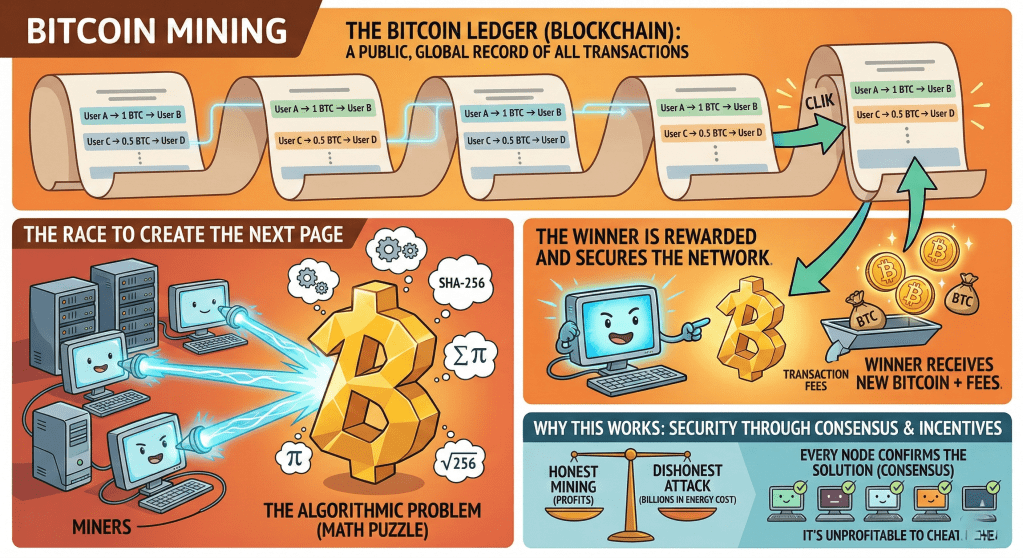

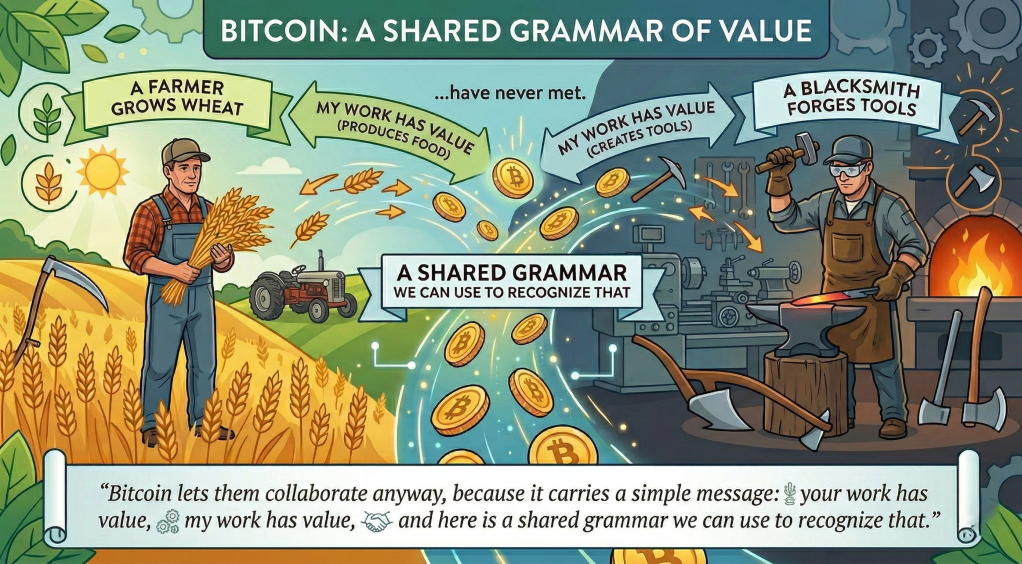

This is what Bitcoin does. And it does it in a way that maps directly onto the problem we’ve been tracing.

Bitcoin removes the intermediary from the ledger. There is no temple. There is no priest. There is no third party who controls the memory and edits it in their own favor. The record of who contributed what is shared, public, and immutable. No one can add a line that says they are owed a cut for the privilege of keeping score.

Without an intermediary extracting rent, there is no structural need to reframe cooperation as transaction. Without a transactional frame, there is no structural incentive for secrecy. The grammar changes, and with it, the kind of sentences that can be composed.

You cannot build an Epstein operation on a transparent ledger. Not because the technology prevents crime through force, but because the language no longer supports the necessary constructions. The dark rooms where leveraged secrets accumulate simply don’t exist in a grammar that records everything openly and permanently. Every satoshi has a history. Every sentence in Bitcoin can be parsed against the actual record. The double meanings that fiat permits, the “consulting fees” that are really payments for silence, the “donations” that are really purchases of legitimacy, Bitcoin’s grammar doesn’t accommodate them.

This won’t make people virtuous. People will always be people. But it changes what the language rewards. A cooperative grammar rewards contribution. A transactional grammar rewards secrecy. We have been speaking the transactional language for five thousand years, and we keep being surprised when it produces what it was designed to produce.

The Epstein files are not the end of a story. They are the latest chapter in a story that began when the first temple priest picked up the first clay tablet and realized that controlling the memory of cooperation was more profitable than cooperating. Every generation since has produced its own version. The names change. The architecture doesn’t.

Until the language does.

Bitcoin is not a better transaction system. It is a different language. One whose grammar remembers what money was before the middlemen got hold of it. A cooperative technology. A shared memory. A way for strangers to work together without handing their trust to someone who will inevitably sell it.

Five thousand years is a long time to speak the wrong language. The right one is available now. It doesn’t require permission to learn. It doesn’t require an invitation to a dinner you’ll regret attending. It just requires the willingness to hear what money was always trying to say before the priests, the kings, the banks, and the Epsteins edited the message.

Money is a language. For the first time in five millennia, we get to choose which one we speak.